In a few weeks, Canadian taxpayers will have filed their income tax returns – and some may have noticed that there were things they could have done last year that would have had a positive impact now. Since we are once again at the beginning of a new year, here are five forward-looking ideas for individuals that could favour capital growth and reduce their tax bill.

Two questions about RRSPs and TFSAs

Because they are such familiar features of our financial landscape, it’s easy to forget that the registered retirement savings plan (RRSP) and the tax-free savings account (TFSA) provide some of the most powerful tax benefits available to Canadians. Here are two specific questions that we might tend to overlook:

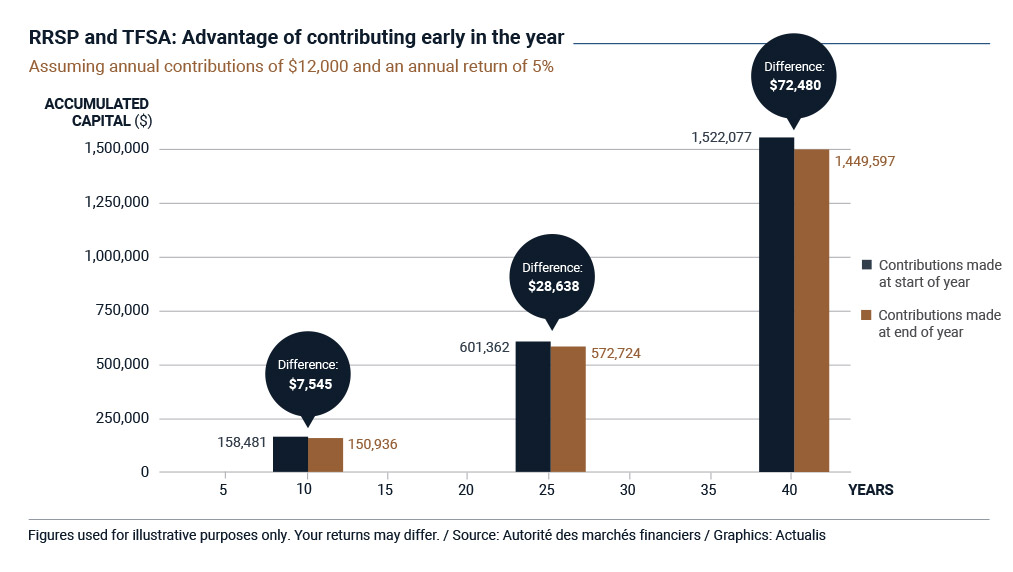

- When is a good time to contribute?

How would you like to find a surprise cheque for some tens of thousands of dollars in your portfolio the day that you retire? Thanks to compounding of tax-sheltered returns, this is what you could gain by making contributions at the start of the year instead of the end of the year, as illustrated by the following diagram. (To learn more about compound returns, read the Actualis article on this topic).

- What investments should go into an RRSP and a TFSA?

The Income Tax Act defines different types of income for individuals, with each type subject to different tax provisions. For example, employment income and interest income are fully taxable, while only half of a capital gain on investment is taxable. Knowing this, which investments should you hold in your RRSP and your TFSA? One rationale, for example, would place interest-bearing investments in a TFSA, since interest income outside of a TFSA would be fully taxable. In contrast, it might be tempting to hold investments with the highest potential for appreciation in a TFSA to shelter them completely from taxes, even though only half of the capital gains would be taxable outside of the TFSA. These topics could fuel an interesting discussion early in the year with your mutual fund representative or financial security advisor. - The forgotten tax benefit: life insurance

Among the rare sources of income that are not usually taxed in Canada, there is one that often flies under the radar: life insurance. This special status can give rise to any number of advantageous tax strategies, including but not limited to estate planning strategies. - Dollar-cost averaging: out-thinking the markets

The fourth quarter of 2018 was a tough time for the financial markets. If you invested a significant chunk of money at the end of September, you might have gotten the uncomfortable feeling that you chose the wrong time to invest. Well, there might be a way of “taking emotions out of the equation” in this type of situation – and when the markets heat up, too. Known as dollar-cost averaging, this approach simply consists of investing a specific sum on a regular schedule – once a month, for example. That way, you would be investing at every phase of a market cycle, with your instalment purchasing more units when prices are low and fewer when prices are high. In mathematical terms, dollar-cost averaging could allow an investor to bring the purchase price down to an average – not the lowest or the highest – while optimizing market exposure. A dollar-cost averaging plan can easily be set up using mutual funds. - Strategies for entrepreneurs

Finally, despite the tax reform that came into force on January 1, which has put some limitations on their fiscal flexibility, business owners still have some attractive tools for optimizing their retirement capital or protecting the wealth they would like to pass along. These include the Individual Pension Plan, which you might want to look at soon if you are in your fifties, as well as various kinds of trusts. These tools involve some complex strategies, but could be financially worthwhile.

Of course, this is only a brief overview. To explore this topic in more depth as the year gets under way, feel free to contact your mutual fund representative or financial security advisor.

The following sources were used to prepare this article:

Actualis, “Are you familiar with the Individual Pension Plan?,” January 2019.

Financial Consumer Agency of Canada, “Main groups of income.”

Autorité des marchés financiers, “RRSP - Registered Retirement Savings Plan: What are the advantages?”

Fiscalistes.com, “Fiducie familiale.”

Investopedia, “Dollar-cost averaging.”

Les affaires, “Entrepreneurs : payez moins d’impôt grâce à votre assurance vie,” June 2016.